mindful banking: a regular person tries move their money out of oil (divesting)

mindful banking: a regular person tries move their money out of oil (divesting)

NOTE: I am a plebe and do not have any financial certifications, this is just what I do. It is not financial or investment advice or product recommendations.

Disclaimer: I am a random person and do not have any financial certifications, this is just what I do with my own funds. It is not financial or investment advice or product recommendations.

In honor of Earth Day (and the world), I wanted to create this post that talks about how I manage some of my money to divest from fossil fuels and how you can, too.

How your checking, savings, and credit cards supports fossil fuel projects (yes, I promise, they do)

When you have money in a bank, it doesn’t just sit there. The bank essentially uses the funds to fund or loan toward other projects—including businesses coming to them and asking for loans. This is why, in part, your money is FDIC-insured.

Banks aren’t required to tell you what or where they’re sending your money, but in December 2023, Wired released an article that highlighted that even just $1,000 in a savings account creates emissions equal to a NYC<>Seattle flight.

Yes, a savings account creates emissions.

The biggest banking and financial institutions that do this are widely reported—you can see that report here. I already knew these banks were bad, and I haven’t banked with a major “big bank” since 2013, but I had a Chase account in college.

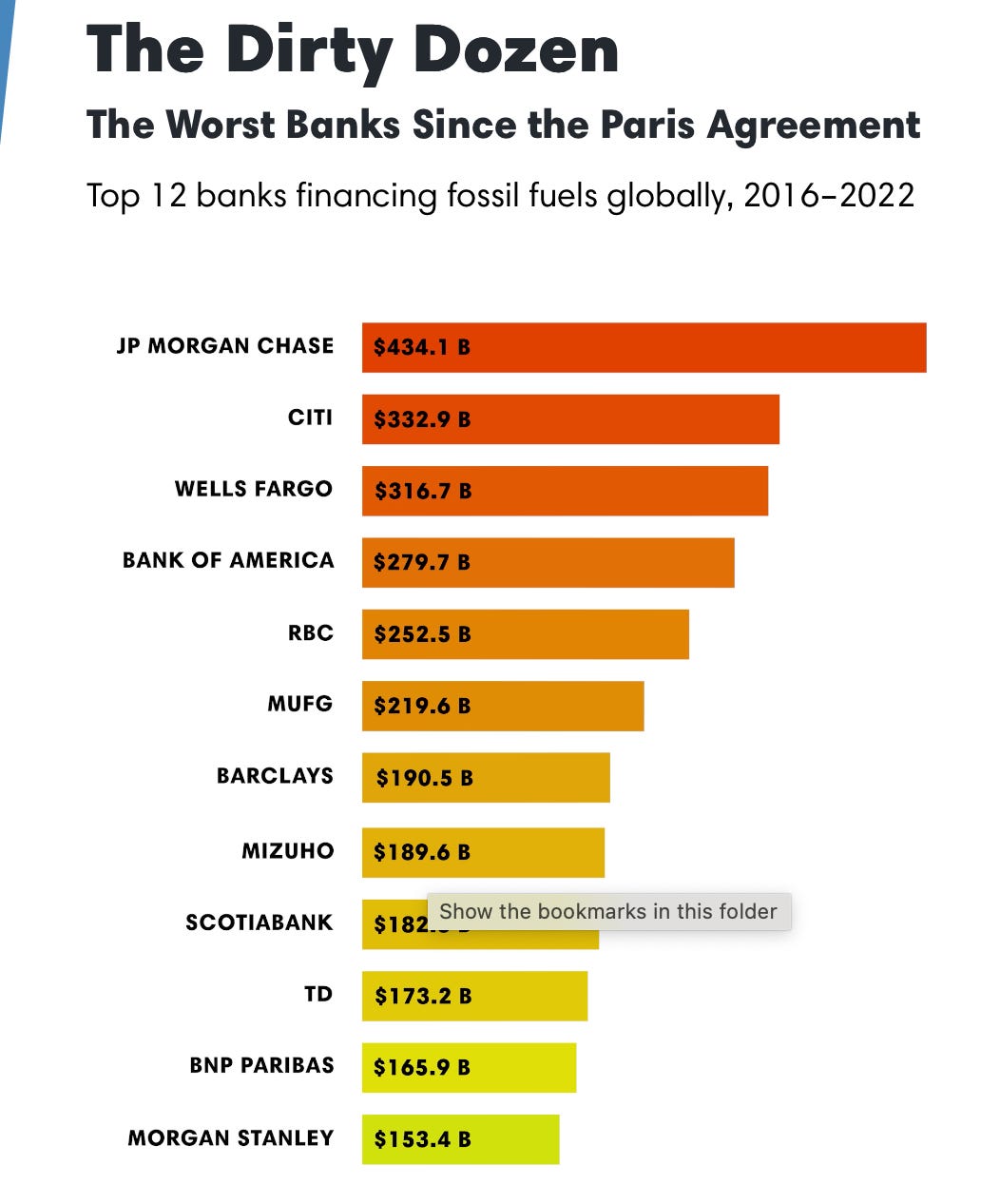

The 14th annual Banking on Climate Chaos report showed that for the first time, Canadian banks are funding the majority of climate-causing chaos

There is also a super cool graphic that shows you directly how much money each bank funnels into different fossil fuel projects and different companies like Exxon Mobil.

The Sierra Club writes, “The report shows that overall, U.S. banks dominate fossil fuel financing, accounting for 28% of all fossil fuel financing in 2022. JPMorgan Chase remains the world’s worst funder of climate chaos since the Paris Agreement. Citi, Wells Fargo, and Bank of America are still among the top 5 fossil financiers since 2016.”

This is especially true for retirement accounts. Basically, almost all retirement accounts involve investments in companies that make or distribute weaponry, oil, fossil fuel projects, or other questionable capitalist behavior. Even options like “sustainable investments” or “ESG” investments are mostly green-washing.

If, like me, reading this makes you feel disappointed and pissed off—well, yeah, I hear that. Thankfully, I figured some ways to improve this for myself, and, hopefully, some of it can help you, too.

How does slow living relate to fossil fuels?

Slow living relates to fossil fuels because, well, living intentionally means thinking about the impact on the planet and the communities most impacted by climate change—which are, without a doubt, people of the Global South, lower-income individuals, queer people, and people of the Global Majority.

I don’t want to make assumptions about you but, I bet, I can safely assume you care about those communities, and, potentially, identify as a part of some or all of those communities.

When we extend the idea of intentionality from ourselves and our choices to the impacts on those around us—whether we know them or not—it can lead us to reconsider choices.

On top of that, I’m not a person who has children, but I often think about a hypothetical. I imagine myself as older and having to explain what I did (or didn’t do) to help protect the planet against climate change. One of the easiest (most passive ways) if you’re privileged enough to have saved money, retirement funds, or investments, to me, is to reconsider who is holding your cash.

Again, I am not a financial expert. Your financial situation is not my financial situation. What you need from a bank account is unique to you.

Also, if you’re interested in finances and care about things like high-yield savings account, you might notice that some of the APY (or the “interest rate” you get from a bank account) are a bit lower than compared to some high-yield accounts.

While slightly lower interest can hurt a little, to me, I’d rather have less interest and. . . have a planet I can live on.

What do all of these banks offer?

Debit cards

A solid app

An interest level between about 2% and 4% APY, depending on the bank.

An easy way to connect to other banks (to transfer money)

A clear commitment to investing in sustainable energy, non-fossil fuel projects, and/or the local economy

My banking top picks — in my personal opinion—listed in alphabetical order

I’ve tried a lot of banks. Seriously. There are years where I’ve switched banks 2 or 3 times because I’m insane. But now, I’m a simpler person who wants to set it and forget it. Before I did, though, I tried out—and liked—all four of these banking options.

Amalgamated Bank

Amalgamated is based in New York and D.C., and they’re a great bank that originally started as a worker’s union—fuck yeah! They do a lot of great things. They don’t invest in fossil fuels, they pay workers $20/hour minimum, all of the people I’ve ever spoken to in person are nice.

Pros

In NYC, and some other cities, they have in-person ATMs and branches for when you need it.

Their new debit cards are made out of recycled plastic and they’re very cute.

They’re local; they offer checks, savings, and investment accounts.

They offer additional programs, like debit cards that support specific charities and round-up donations.

Cons

They recently got a new digital banking experience that’s much better, but their Android app, while functional, is certainly the least beautiful on this list.

They do charge some fees that other banks on this list don’t.

Atmos Bank

Atmos is a digital-only bank, meaning you need a smartphone or the web app. They offer joint-checking now, which is cool.

Pros

Good app

If you make a monthly donation to one of their selected nonprofits, you can earn up to 3.5% APY on your savings.

You can have savings accounts—up to 6 so you can keep your finances organized. As someone who banked with Ally and Capital One 360 for a long time so I could separate out my budget into “rent", “holiday spending,” etc., this is a great feature.

Their work funds local solar energy projects across the United States

Cons

I think they don’t offer check ordering, which can be annoying if you have an old-fashioned New York landlord

They do have fee-free ATMs, but they don’t reimburse any ATM fees

Future Green

Future Green came out a couple of years ago—you might have seen the NYC subway ads offering to reimburse you for transit fare—but for a year or two they were just an iOS mobile app, which I didn’t love.

Now, thought, times have changed, and in addition to both iOS and Android apps, they offer an optional physical debit card they’ll send you in the mail.

Pros

Current interest rate is 2.72% APY.

They offer cash back! For specific companies and things like using public transit, you can get as much as 5% back on your purchases. I use this for subway fare, and it’s awesome.

They have a really sleek, cute app.

The app updates super fast with any spending, so your balance is accurate.

This is both a pro and a con—they have a “rewards” program that links to companies you can get extra cash-back on. This is great, but it does encourage spending and consumerism in its own way.

No fees.

Cons

There’s no way to access the banking features without a mobile app. So, in my smartphone-less days, this would have been totally unusable for me.

The debit card took a while to arrive when I ordered it.

There’s no savings account in addition to the main debit card account.

They don’t reimburse fees the way Walden Mutual does.

This is both a pro and a con—they have a “rewards” program that links to companies you can get extra cash-back on. This is great, but it does encourage spending and consumerism in its own way.

Walden Mutual Bank

Walden Mutual is a bit of a rarity in that their banking is based on local community impact. Specifically, Walden Mutual cares most about investing in the New York and New England area’s local food economy, be it farmers markets, food coops, or small farm stands on the road.

Pros

They have a great app.

No fees and a one-cent account minimum.

Their interest rate is solid—3.05% APY, and anything between $10K and $100K earns 4.05% APY

They publish a cool annual report of their impact on the local food systems

They have really, really good customer service—I had to speak to someone once with a question and they were incredibly responsive over both email and phone.

They have a personal touch—they send you a business card of a real person you can reach at their bank.

Most of the workers are based in Concord, NH and invested in the community there.

They also have “partner perks,” which are rewards and cash back for certain (mostly local food) companies.

They reimburse up to $15 a month of ATM fees—the only bank on this list to do so.

It’s very easy to link bank accounts to transfer money.

Cons

They don’t offer a separate account for savings at the time of writing.

~~~

If I had to pick just one, I’d probably go for Walden for most of my needs and Atmos if I needed separate savings or joint-checking accounts. That being said, I do use Future to get the most cash back on all the transit I use.

Additionally, if these banks don’t suit your needs, I recommend checking out Bank.green to search for banks in your country, area, or based on your own needs. You can also use this link to check if your bank fuels the climate crisis (which it probably does).

What about retirement accounts?

Last year, I spent about four months trying to find a certified financial planner (CFP) who I could meet with to help me evaluate my retirement accounts.

Most retirement accounts offered by employers, like 401(k)s or 403(b)s, provide a pre-set selection of what you can invest in, like a menu. It’s based on the fees your employer pays to the investment company—whether it’s Empower, Vanguard, Schwab, Fidelity, etc.

When I started my most recent full-time job that offered benefits, which was in 2022, I was basically only able to invest in individual funds, and they were pretty much all fueling the climate crisis. I know because I would take the “ticker” (like APPL) and run it through one of my favorite financial websites, Fossil Free Funds.

“BuT iSn’T ESG iNveStMeNts wOkE bUlLshIt?”

So, asides from the Republicans who get mad when we consider using morals to impact the free market economy, there is a shit-ton of greenwashing among 95% of what I’d consider “fossil-free” or ESG—environmental, social, or governance—responsible funds. That’s true. It’s super disheartening.

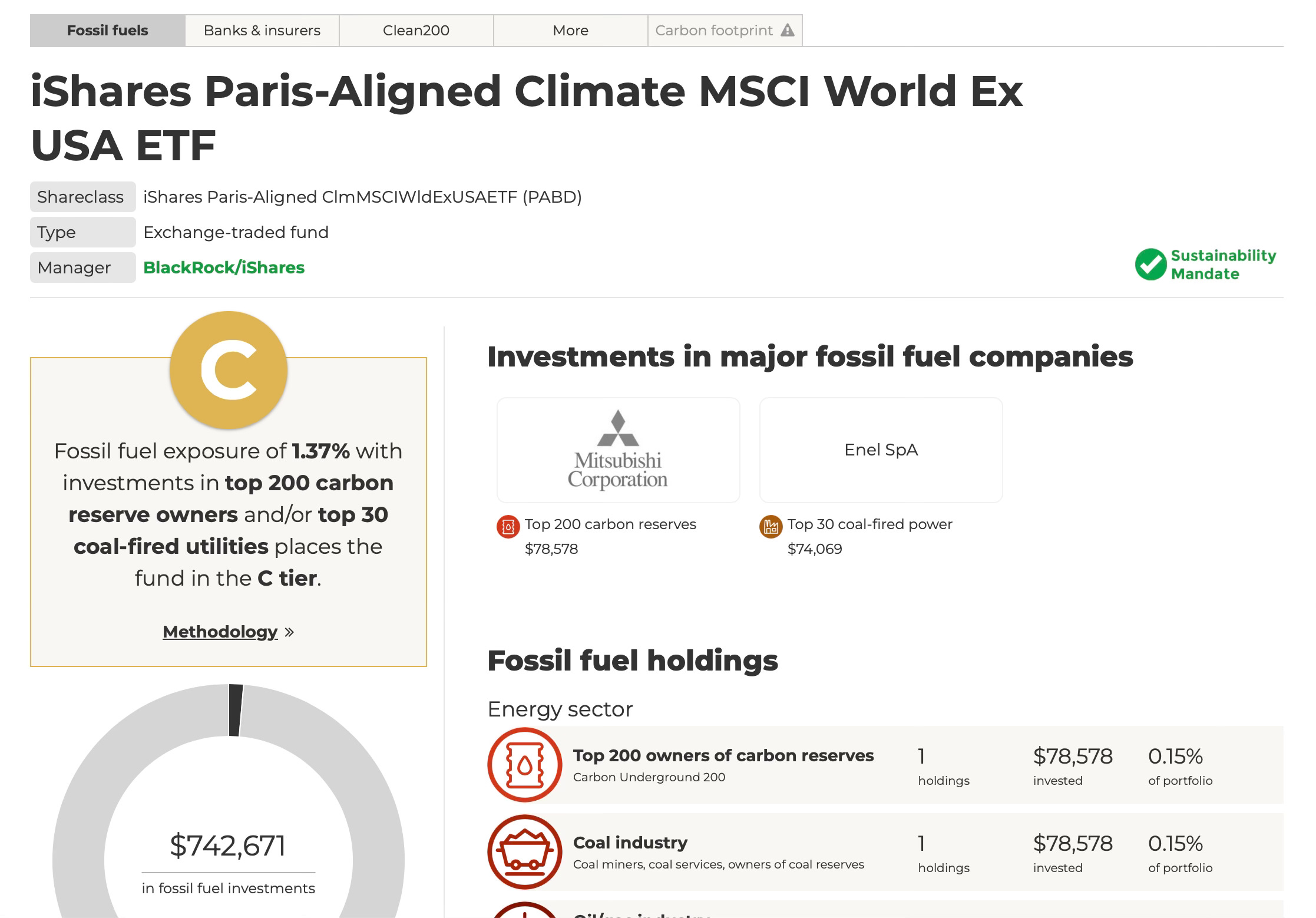

Here, for example, is what happens when you run an “ESG” fund through Fossil Free Funds. This fund is by iShares, which is also connected to Black Rock, one of the worst climate crisis offenders.

Ironically, this fund is called the Paris-Aligned Climate MSCI world ex USA exchange-traded fund. As in, The Paris Agreement. As in, stopping our global warming from going over 1.5 degrees celsius.

The “C” is the overall rating for the climate cleanliness of the fund. You can see if it has a sustainability mandate—this one does!—which means sustainability is, ostensibly, a value of the company. You can also see how much money is invested in the overall portfolio.

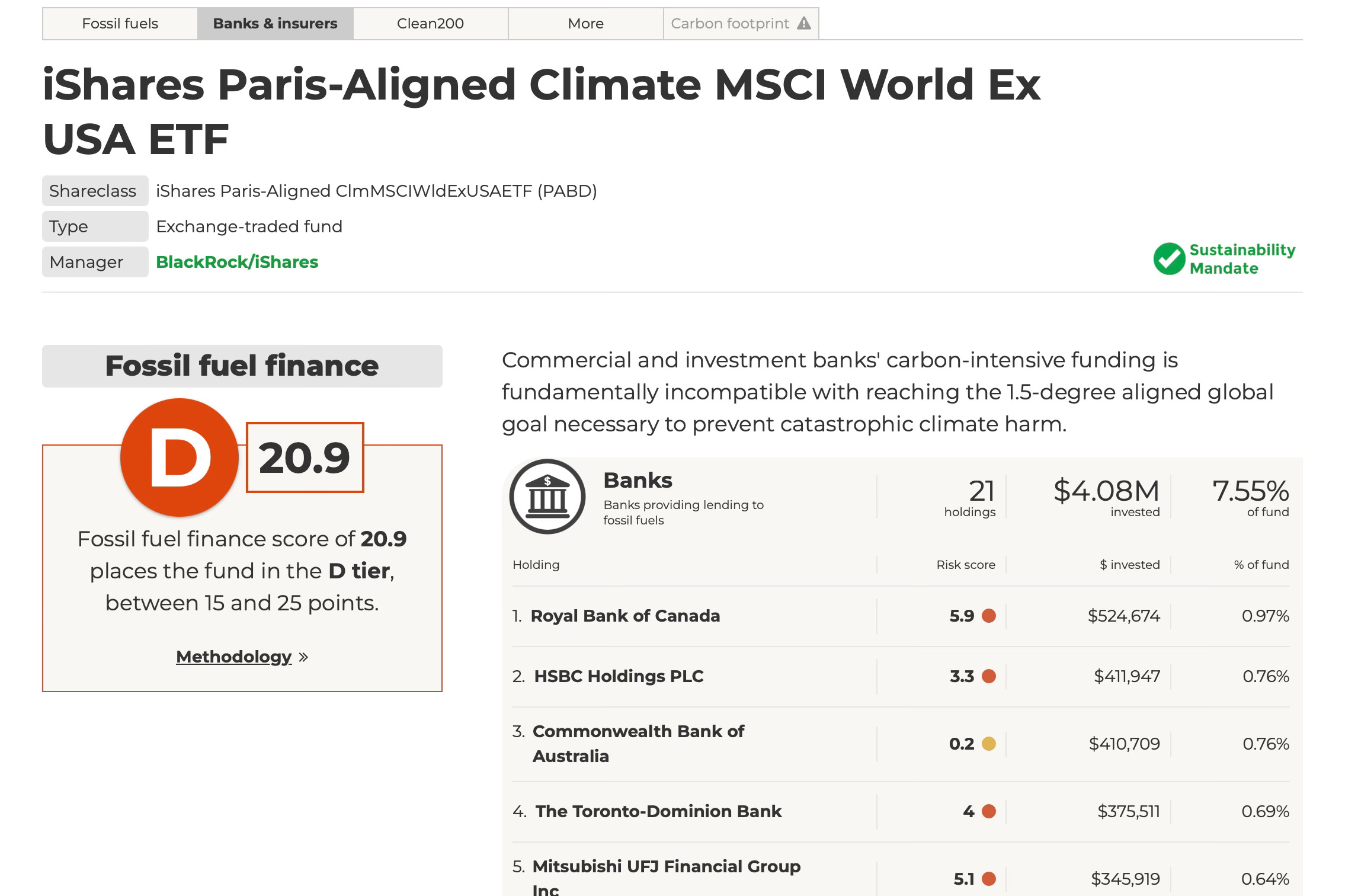

You can also see which banks and insurers are most invested in the fund by clicking on “banks and insurers.” Let’s take a look. . .

Royal Bank of Canada and HSBC are among the biggest banks involved in this fund.

Okay, so you get it. Investments are mostly covered in oil-soaked blood money, so what’s a person to do?

Well, as a non-wealthy person, I wasn’t sure. Most financial planners charge a lot of money for their time to the point that it didn’t make sense for me to hire them.

Additionally, while there are some great companies—like Calvert, Green Century, or Green Alpha where I did actually speak to people—that offer green investments if you let them actively manage your funds, I, personally, don’t believe in having my funds actively managed. (It hasn’t been shown to really be more effective than passive investing, which is my jam.) Again—that’s my opinion, this is not financial advice.

Now, the one big advantage to using an actively managed fund is that there are some great sustainable funds with lower fees, but they have higher minimum account investments.

For example, Fund A - Green Choice might have a fee of 2% but you can invest with just $1000. Fund B - Fancy Green Choice might have a fee of only 0.5%, but you need a million dollars to buy into it.

An investment firm or fund manager like some of the ones I linked above can get you access to these higher-minimum funds because they essentially pool the money of all of their customers together. I think, if you have a lot of money to invest, these companies may be worth it. But for me, as someone with less than $100,000 in investments, the fees of working with an investment firm outweigh the benefits.

But I’ll tell you what I ended up doing for my own finances. After talking to four or five CFPs or management firms, I decided the fees weren’t worth it. Then. . . I found it.

Carbon Collective is a company that offers sustainable investments for individuals, retirement accounts, and companies. They also have a great theory of change page that’s short, sweet, and thoughtful I’d encourage you to check out.

I have multiple retirement accounts (from leaving multiple jobs), so I did roll-overs with each of them. (My accounts were all at Charles Schwab, so it was easy.) You might have to call your bank to initiate the rollover, but it’s a process that sounds scary and, in fact, is pretty easy and painless. It takes like 15 minutes. On the rare occasion, you might have to fill out a form and email it to your bank, but most of the time it can all be done direct on the new company—in my case, Carbon Collective’s—website.

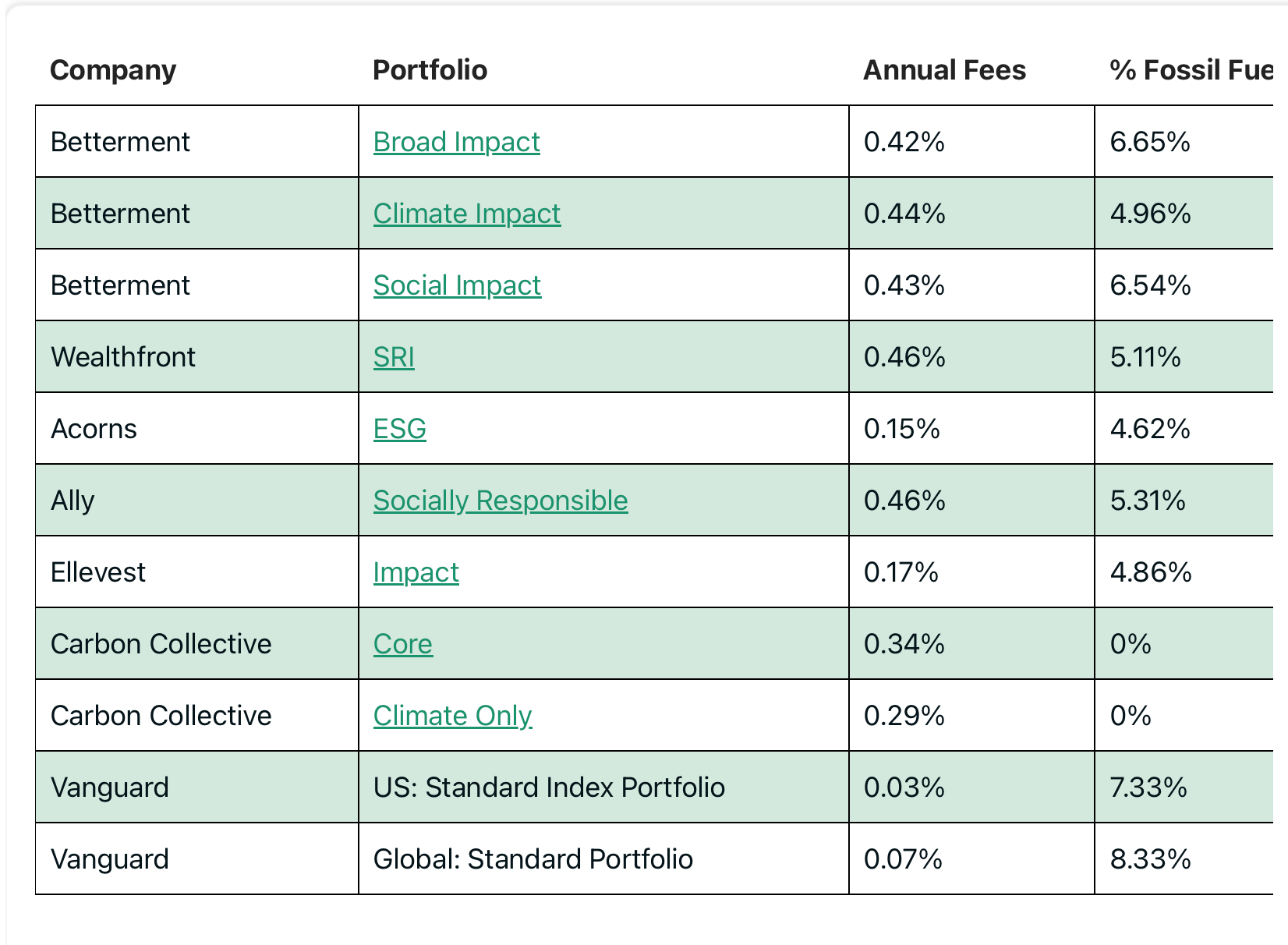

Here’s even a great chart from their site that shows how most of the “ESG funds” offered by big banks just fucking suck.

There’s even a company that will help you with your rollovers that I have personally used called Capitalize. (When I used it, it was free; I think now, there’s a free and a paid model.)

Getting started is way easier than it feels

I know 99% of my friends avoid financial stuff, and I get it. It’s boring. It involves lots of terms. It involves talking to bank people, and most people I know don’t want to talk to anyone, anyway. But, at least for me, it helps me sleep easier at night, and it makes me feel a bit smug when I see signs about how Chase Bank and Black Rock suck ass to know that I have nothing to do with them anymore.

I’d love to know—how does climate change impact your finances? Have you divested your own money from fossil fuels?